How to Use Financial Statements and Ratios

Warning: Use of undefined constant user_level - assumed 'user_level' (this will throw an Error in a future version of PHP) in /home1/accounz1/public_html/blog/wp-content/plugins/ultimate-google-analytics/ultimate_ga.php on line 524

| << Accounting System Structure – Quick Reference |

This post talks about how to make use of the information in Financial Statements. Those statements are really the results of past operations. It is important to use this information to be proactive and look to the future to predict results and to set goals, expectations and budgets based on the evidence provided from the past.

Time analysis is the most important tool you will use in analyzing your Financial Statements. It is essential in managing and securing resources because it can quickly pinpoint changes that indicate errors or fraud as well as the unexpected changes that might require adjustments to cash planning and/or operations.

The first Statement to look at in your personal checking accounts is the comparison Trial Balance. This Statement is very important, it shows the amounts posted to each account month by month complete with totals at the end. The month to month analysis is extremely important for verifying your numbers before you start with ratio analysis.

You can either show all accounts on this Statement or you can limit it to Income Statement Accounts, that is why you should learn how to save more money. I choose to include both types of Accounts so I can track the changes in Financial Position provided by the Balance Sheet Accounts, you may find these checking account tips and software pretty much useful for both personal and business bookkeeping. If you still need some kind of help, we suggest to contact the following website https://atlanticunionbank.com/business/lending/lines-of-credit/.

I’ve added a few entries to the Comparison Trial Balance Report from posts # 7 and 9. You can see that the monthly changes in Rent Expense for Oct and Nov will catch your attention, click here for more information about personal and business loans.

| Account | Description | … | Jun | Jul | Aug | Sept | Oct | Nov | Dec | Total |

| 1000 | Checking | … | -$3,000 | $-3,000 | $-3,000 | -$3,000 | -$3,000 | -$3,000 | -$3,000 | $-21,000 |

| 2000 | Accounts Payable | … | $0 | $0 | $0 | $0 | -$3,000 | $3,000 | … | $0. |

| 7000 | Rent | … | $3,000 | $3,000 | $3,000 | $3,000 | $6,000 | $0 | $3000 | $21,000 |

| Totals | … | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

**This example starts with June because of space limitations here. The additional entries for all months except September are not included in the Income Statement or Balance Sheet, I’ve only added them here for illustration.

Let’s start with Financial Ratios by looking at the Income Statement and its ratios.

Income Statement:

The Income Statement gives you a good overview of your Expenses in relation to your Revenue, more people than ever are using mortgage brokers . It can also help to pinpoint potential problems.

As the dollar value of Sales changes, the dollar values of Costs of Goods and Expenses should also change. By tracking the changes in dollar values in terms of percentages of sales, you can more easily evaluate whether changes in dollar amounts are reasonable, Finding the best personal loan

The percentages are based on a Percentage of Sales. So, Gross Profit Margin = Gross Margin/Sales, Net Profit Margin = Net Income(Profit)/Sales etc.

Know your percentages. Watch your trends over time, both as they accumulate throughout the fiscal year, and as they compare month to month and year to year. Percentages can also be compared to industry ratio standards to measure your results against others in your industry. Make sure that your business is aware of the VoIP Setup Guide and other systems to help your business have success.

Some expenses like wages and payroll taxes, or general office expenses are more meaningful when grouped together to find a percentage of the group rather than as a single line item. Contact this Gst registration Service Singapore to give you better business finance information.

This is the Income Statement that developed through the progressive post entries.

| Income Statement | % of Sales | |||

| Sales | $50,000 | |||

| Cost of Goods Sold | $0 | 0% | ||

| ———— | ||||

| Gross Margin | $50,000 | 100% | Gross Profit Margin % | |

| Rent | $3,000 | 6% | ||

| Office Supplies | $150 | |||

| Subscriptions | $300 | |||

| Utilities | $125 | |||

| Fuel | $275 | |||

| Repairs & Maintenance | $500 | |||

| Credit Card Interest | $50 | |||

| ———– | ||||

| Operating Expenses | $4,400 | 9% | ||

| ———– | ||||

| Operating Income | $45,600 | 91% | Operating Profit Margin % | |

| Other Revenues and Expenses | $0 | |||

| Net Income | $45,600 | 91% | Net Profit Margin % | |

This is a very limited Income Statement Example built from very few entries, but even with the information available, it gives useful information. There is also obviously a problem with this Income Statement, it has no Cost of Goods Sold to relate to Sales. In this case, we’re either missing information or we’re violating the Revenue Principle and recording Sales before they’ve been earned. (Pinpointed Problem) It’s also crucial in the UK that if you take payments online that you have PCI DSS certification as it’s a legal requirement so make sure you have that in place if you are in the UK.

Malaysian online casino w88 malaysia is now the official sponsor of crystal palace football team in the english premier league. Malaysian online players can feel safe knowing that they are playing in a trusted online casino.

Gross Margin is also called Gross Profit or even Gross Profit Margin and the terms Income and Profit are also often used interchangeably. Just be consistent in your terminology so that users will not be wondering if there is a difference in meaning if you use a different term.

**Comparing your business against other businesses in your industry is called Benchmarking. There are a number of free or fee based benchmarking services online.

Remember that the Income Statement is a Yearly Statement, all its accounts are reset to zero at the end of each year and the difference (Net Income) is transferred to the Equity section of the Balance Sheet as either Retained Earnings (for Corporations) or as Owners Capital (for all other types of entities). Contact this IGCSE tuition centre nearby for more education information.

Balance Sheet Ratios:

The Balance Sheet gives you a good overview of your financial position at any point in time. The Balance Sheet is not a Yearly Statement, it is a cumulative statement whose accounts retain their balances from the beginning to the end of the entity.

All Assets and Liabilities on the Balance Sheet should contribute to increasing the value of the entity. If they are not contributing, they might need to be liquidated.

The “Current” sections of the Balance Sheet are important to keep track of because it will be Current Assets which will pay off Current Liabilities, you want to make sure you have at least as many Current Assets as Current Liabilities. The items in the Current Sections are considered to be the most liquid, that is, they are the most likely to be able to convert to cash at (or close to) their stated value, also the checking system is important, henc (but still may use other similar services) in 2021-2022.

Two Assets to pay particular attention to are Accounts Receivable and Inventory. Receivables are an essential tool in doing business, they finance purchases for your customers but it is important to watch their aging and balances to make sure you are not extending credit to customers who are unable to pay, the guys at arcct.com offers poor credit loans and other financial programs for people with bad credit but that can change with help from a mortgage broker Auckland. Watch Inventory turnover to make sure you that your inventory is selling and that you are not carrying obsolete or otherwise unsellable items. You can also get help from Mortgage Broker Northern Beaches as they have the best Expert Mortgage Brokers Servicing the Northern Beaches.

An installment loan is a modern type of loan which is repaid at a certain period of time. Normally, you can pay the loan with one or two payments. The term of the loan may vary from a few months to over 20 years. Installment loans for people with bad credit are extremely easy to obtain with ARCCT and very effective and you can learn how to bounce back with a recovery advice for your small business to manage to save your finances.

Installment loans are becoming increasingly popular all across the world, especially as most people who are in urgent need of money choose to apply for a bad credit installment loan instead of trying to get a traditional loan. Instead of waiting up to three days for the money to come, you can now have the requested amount in your account as soon as the next business day. Regardless of the reason, whether it’s an expensive birthday present, a health insurance policy or an urgent bill, installment loans for bad credit could prove invaluable. Best of all, these loan and short term loans with monthly payments can be taken even with a poor credit history. If you have bad credit here you can get Fast Cash Now, but before getting cash you can compare credit cards to see which one is the best option for you.

Purchases that your Vendors finance for you are liabilities called Payables. Payables and other Liabilities are essential for financing current operations and growth but keep close track of their related interest and fees to make sure their costs do not exceed their benefits, but when using outsourcing services for your business is better to get a business process outsourcing insurance from great insurance bpo providers which could help a lot when managing these kind of services.

| Balance Sheet | |||

| Assets | |||

| Current Assets | |||

| 1000 | Checking Account | $44,350 | |

| Fixed Assets | |||

| 1500 | Office Equipment | $1,300 | |

| 1520 | Office Furniture | $1,650 | |

| ———— | |||

| Total Fixed Assets | $2,950 | ||

| ———— | |||

| Total Assets | $47,300 | ||

| Liabilities and Equity | |||

| Current Liabilities | |||

| 2000 | Accounts Payable | $1,700 | |

| ———— | |||

| Total Liabilities | $1,700 | ||

| Equity | |||

| Net Income | $45,600 | ||

| ———— | |||

| Total Liabilities and Equity | $47,300 | ||

Some important financial ratios to keep track of are:

Current Ratio which is Current Assets/Current Liabilities this ratio should always be at least 1

Quick Ratio = Current Assets – Inventory/Current Liabilities this ratio removes Inventory from Current Assets because Inventory is usually the least liquid of the Current Assets.

The next ratios are approximations, they give you a good idea about what they are measuring. They are general enough to give you an idea about where to look for trouble items but they are not specific enough to be fool proof.

Inventory Turnover = Sales/Inventories this ratio gives you a rough idea of how many times your inventory is sold and restocked. Of course, it does not specifically identify inventory items so there may be items that are not selling but it does tell you how well your sales are covering your costs. Take a look at https://www.stocktrades.ca/cpp-payments/ and how you can get reports on your investments.

Days Sales Outstanding = Receivables/(Sales/360) this ratio gives you a number that represents aging of your receivables. If your terms are net 30 days and this ratio gives you a number of 45 or more, then it is a good indicator that you should watch your collections carefully.

Fixed Asset Turnover = Sales/Net Fixed Assets (Fixed Assets – Accumulated Depreciation) this ratio provides an idea of how effectively your Fixed assets are contributing to operations. This ratio can be slightly misleading because Assets are carried at book value rather than market value which might scew this ratio depending on the age of the Assets.

Total Assets Turnover = Sales/Total Assets this ratio provides an idea of how effectively your total assets contribute to operations and increases in entity value. Although this ratio will have the same problems as the Fixed Asset Turnover ratio both of these ratios are still important to recognize and watch for trends.

As I said at the beginning of this post, know your percentages (ratios) watch them carefully. You should use them to your advantage for predictions, corrections and budgets for your current and future operations and policies.

© 2008 – 2010 Erin Lawlor

<< Accounting System Structure – Quick Reference

**disclaimer: All information posted on this blog is from my own experience and training. The guidelines I present are general and in my experience, standard practice. I do not write with authority from any Accounting Standards Boards.

Accounting Structure – Quick Reference

Warning: Use of undefined constant user_level - assumed 'user_level' (this will throw an Error in a future version of PHP) in /home1/accounz1/public_html/blog/wp-content/plugins/ultimate-google-analytics/ultimate_ga.php on line 524

| << Accounting Journals and Ledgers | How to Use Financials and Ratios >> |

This post is a quick overview of subjects covered in more detail in other posts. I usually like to see a quick version so I am trying to present that option to others as well.

The Double Entry Accounting System collects, organizes, summarizes and reports on Financial Transaction data.

Financial Transactions: Exchanges of things of value.

There are three basic questions that must be answered for each financial transaction, they are:

- Question 1. How much money changed hands? What is the value of this exchange?

- Question 2: How was the money used? What was either gained or paid for by this exchange?

- Question 3: Where did the money come from? What is the source of funds in this exchange?

Example:

- Answer 1: 3,000.00

- Answer 2: Rent

- Answer 3: Checking Account

The answers for each of the financial transaction questions are recorded in Journals digital wallets vs credit cards. Journals have a grid format with a varying number of columns but to start, for professional accountant, we’ll use three columns. If you think this is too much for you to do on your own, then consider doing cloud accounting to make organizing your financials much easier.

See which clouds can be connected to here to have the connectivity that you can trust.

The descriptions that answer questions 2 and 3 are always entered on separate lines to the left of the two numeric columns.

The amount associated with question 2 is entered on the same line as its description and it is always answered in the left (debit) numeric column. The amount associated with question 3 is entered on the same line as its description and it is always answered in the right (credit) numeric column.

General Journal Example:

| Description | Debit | Credit |

| Rent | $3,000 | |

| Checking Account | $3,000 |

To ensure that both sides of the transactions are recorded, Total Debits must always equal Total Credits.

To keep the Chart of Accounts manageable and meaningful, it is important to strike a balance between having a long specific list and a short general list. To accomplish this objective, the Chart of Accounts should have descriptions for types of things, and not for specific things. You want the high volume accounts to be specific enough to be useful but not too specific because the fewer accounts you have the better overall picture you can have. Find Payroll Outsourcing at B Accounting

Chart of Accounts Organization: The Chart of Accounts is organized using three different methods.

- First: Accounting Types

- Second: Order of Liquidity – the ease of converting to cash

- Third: Account Numbers

The listing below shows the Chart of Accounts organization along with sample Account Number Ranges.

- Assets: 1000’s

- Current Assets 1000 – 1499

- Fixed Assets 1500 -1999

- Liabilities: 2000’s

- Current Liabilities 2000 – 2499

- Long Term Liabilities 2500 – 2999

- Equity: 3000’s

- Revenue: 4000’s

- Costs of Goods Sold: 5000’s

- I leave the 6000’s open to allow for a Cost of Goods Sold Subtype

- Expenses: 7000’s

- Other Revenue: 8000’s

- Other Expenses: 9000’s

Journals and Ledgers:

There are two types of Ledgers and Journals in the system, General and Subsidiary. If you recall from above, I said that Accounts should only be created in the Chart of Accounts/General Ledger to describe types of things not individual things themselves. Well, in some cases especially in the case of cash substitutes like Accounts Payable and Accounts Receivable more detail is required. So, to maintain the summary nature of the Chart of Accounts/General Ledger and to provide more detail, a Subsidiary System of Journals and Ledgers was developed, while also using other systems as a Certification Tracking System to track the employees and their improvement in a company, while also giving them better chances to learn their own progress.

General Ledger: The General Ledger is the combination of the Chart of Accounts, Account Balances and Accounting Periods. The General Ledger maintains the summary balances of ALL financial transactions.

The General Ledger adds the essential organizational element of Time (Accounting Periods) to the Grain Accounting System, so in addition to the original three organizational methods of the Chart of Accounts, the General Ledger is organized in four ways.

- 1. Accounting Type

- 2. Order of Liquidity

- 3. Account Number

- 4. Accounting Periods

Accounting Periods are generally date/time intervals of Months, Quarters and Years. The element of time is essential to accounting. It provides the ability to report balances for any given accounting period as well as the ability to compare the results of different accounting periods against each other.

If the system is going to organize around accounting periods, then we need to add dates to the data we gather with transactions. There can be a variety of dates that are relevant to a transaction, the transaction date, the invoice date, the due date, the expiration date etc. but for purposes of this post, the date we’ll focus on is the transaction date.

The Journal transaction grid introduced in the previous section needs to be expanded to 5 columns to accommodate the new data requirements of date and account number.

General Journal Example:

| Transaction Date | Account | Description | Debit | Credit |

| 9/01/08 | 7000 | Rent | $3,000 | |

| 1000 | Checking Account | $3,000 |

Subsidiary Journals and Ledgers: The two most common Subsidiary Systems are:

- Accounts Payable

- Accounts Receivable

All financial transactions that involve a general ledger account with an associated subsidiary ledger must be recorded in that subsidiary ledger first.

Subsidiary Journal:

| Accounts Payable Journal | |||||||

| Subledger Account | Invoice # | Transaction Date | Ref | GL Account | Description | Debit | Credit |

| ACEC | 123_908 | 9/01/08 | 55 | 2000 | Ace Credit Card Corp. | $1,700 | |

| 1520 | Chair | $750 | |||||

| 1520 | Desk | $900 | |||||

| 7300 | Credit Card Interest & Fees | $50 | |||||

Notice that the Subsidiary Journal uses more columns than the General Journal. It uses the extra columns to track data that is specific to the Subsidiary Ledger as well as to the General Ledger.

General Journal:

The system requires that all financial transactions have an entry in the General Journal as well as in the General Ledger. So, once the entries are posted to the Subledger Journals, they are then summarized and posted to the General Journal.

| General Journal | ||||||

| Transaction Date | Jrnl | Ref | Account | Description | Debit | Credit |

| 9/01/08 | AP | 55 | 1520 | Furniture & Fixtures | $1,650 | |

| 9/01/08 | AP | 55 | 7300 | Credit Card Interest & Fees | $50 | |

| 9/01/08 | AP | 55 | 2000 | Accounts Payable | $1,700 | |

Notice the new columns in this General Journal example, they are cross referencing entries to show where the transaction was originally recorded. The Jrnl in this example says AP = Accounts Payable and the Ref (55) is the same as in the AP Journal example above. The Ref is the transaction reference number and will increment for each transaction.

Ledger Examples:

Each financial transaction is recorded in the appropriate Journals and then summarized and posted to the Ledger Accounts.

| Accounts Payable Subledger | Account: ACEC | |||||

| Transaction Date | Jrnl | Ref | Description | Debit | Credit | Balance |

| Beginning Balance | $0 | |||||

| 8/01/08 | AP | 23 | 123_0808 (invoice) | $2,500 | $2,500 | |

| 8/31/08 | CD | 37 | 123_0808 (payment) | $2,500 | $0 | |

| 9/01/08 | AP | 55 | 123_0908 (invoice) | $1,700 | $1,700 | |

| General Ledger | Account: 2000 | |||||

| Transaction Date | Jrnl | Ref | Description | Debit | Credit | Balance |

| Beginning Balance | $0 | |||||

| 8/01/08 | AP | 23 | Accounts Payable Invoices | $2,500 | $2,500 | |

| 8/31/08 | CD | 37 | Cash Disbursements | $2,500 | $0 | |

| 9/01/08 | AP | 55 | Accounts Payable Invoices | $1,700 | $1,700 | |

The Subsidiary Ledger (Subledger) is like the General Ledger/Chart of Accounts in that it contains a list of Accounts specific to its purpose. The Accounts Payable SubLedger contains a list of AP Accounts and their balances.

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

The Total Balance of each Subledger must equal the balance of its related General Ledger Account Balance. All financial transactions are recorded in the General Journal and the General Ledger and only the transactions with a gl account that has a related Subledger are posted to a Subsidiary Journal and Ledger.

If the Subledger does not Balance with its related account on the General Ledger, it means that there may be entries in either the Subledger or the General Ledger that are not in the other. They should each have matching entries and there should be no entries made to the General Ledger for an Account with a related Subledger that are not also made to the Subledger and vice verse, and using accounting services from the accounts payable services providers could be really helpful to help you automatize the accounting services of your company.

© 2008-2010 Erin Lawlor

Next: How to Use Financial Statements and Ratios >>

<< Accounting Journals and Ledgers

**disclaimer: All information posted on this blog is from my own experience and training. The guidelines I present are general and in my experience, standard practice. I do not write with authority from any Accounting Standards Boards.

Accounting Journals and Ledgers – Transaction Posting

Warning: Use of undefined constant user_level - assumed 'user_level' (this will throw an Error in a future version of PHP) in /home1/accounz1/public_html/blog/wp-content/plugins/ultimate-google-analytics/ultimate_ga.php on line 524

| << Percentage of Completion and WIP Statement | Accounting Structure -Quick Ref >> |

The process of gathering and storing Financial Transaction data in the Accounting System is accomplished through the use of both:

- Ledgers: which maintain Account Balances

- Journals: which maintain the line by line detail of each Transaction.

Ledgers:

I’m starting with Ledgers because we’ve gone through the basic organization of the Accounting System from Double Entry (debit/credit) Transaction Posting, to the Chart of Accounts and finally the General Ledger. I’ll stay on the topic of the General Ledger first and then back up to the Journals where each transaction is originally posted.

In Accounting, there are two types of Ledgers, the General Ledger (Book of final entry) and Subsidiary (Sub) Ledgers. The Accounts for the General Ledger come from the Chart of Accounts. The Accounts for the Subledgers depend on the specific purpose of the Subledger.

If you remember in the “Chart of Accounts – Basics”, I said that Accounts should only be created to describe types of things not individual things themselves. Well, in some cases especially in the case of cash substitutes like Accounts Payable and Accounts Receivable more detail is required. So, to maintain the summary nature of the Chart of Accounts/General Ledger and to provide more detail, Subsidiary (Sub) Ledgers were developed.

Everything that is posted into Subledgers is also posted into the General Ledger and they act together to provide progressive levels of detail/summary.

The two most common Subledgers are:

- The Accounts Payable Subledger: which maintains a list of Vendors (or creditors) and their individual Account Balances. Each individual Vendor represents a Subledger (Accounts Payable – Vendor) Account.

- The Accounts Receivable Subledger: which maintains a list of Customers and their individual Account Balances. Each individual Customer represents a Subledger (Accounts Receivable – Customer) Account. Card payment providers offer reliable solutions for businesses to accept card payments from customers.

Each Subledger relates directly to a General Ledger Account that requires more detail than the General Ledger can offer. These GL Accounts are often referred to as control accounts. The Balance of a Control Account should always be equal to the total of its related Subledger Account Balances. As you can see, the total of the Accounts Payable Subledger below equals the Balance of the related General Ledger Accounts Payable Account.

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

The listings above are Ledger Account summaries. Both the General Ledger and the Subledgers actually have a more detailed section for each Account. Those sections include summarized entries and balances along with references indicating which journals those entries originated in.

The tables below show an example of a Subledger Account and an example of the corresponding General Ledger Account.

| Accounts Payable Subledger | Account: ACEC | |||||

| Transaction Date | Jrnl | Ref | Description | Debit | Credit | Balance |

| Beginning Balance | $0 | |||||

| 8/01/08 | AP | 23 | 123_0808 (invoice) | $2,500 | $2,500 | |

| 8/31/08 | CD | 37 | 123_0808 (payment) | $2,500 | $0 | |

| 9/01/08 | AP | 55 | 123_0908 (invoice) | $1,700 | $1,700 | |

| General Ledger | Account: 2000 | |||||

| Transaction Date | Jrnl | Ref | Description | Debit | Credit | Balance |

| Beginning Balance | $0 | |||||

| 8/01/08 | AP | 23 | Accounts Payable Invoices | $2,500 | $2,500 | |

| 8/31/08 | CD | 37 | Cash Disbursements | $2,500 | $0 | |

| 9/01/08 | AP | 55 | Accounts Payable Invoices | $1,700 | $1,700 | |

Because there can be multiple Subledgers, there are also multiple Journals. The Jrnl field indicates which journal the entry came from. The AP’s in the jrnl field mean that those entries came from the Accounts Payable Journal and the CD entry came from the Cash Disbursements Journal which is the journal that maintains detail for Cash Outflows. The Jrnl and Ref field together give a cross reference that enable the user to access more detail about each entry. Learn how to start fundraising with https://norgesbriketten.no/dugnad-tjene-penger-klassetur/ best place for Norwegian voluntary and communal work.

Journals:

All financial transactions are recorded in Journals. The Journal maintains each individual transaction line by line. Just as there are two types of Ledgers, there are also two types of Journals: The General Journal and the Subsidiary Journals. Most entries will originate in Subsidiary Journals, however, if none of the GL Accounts affected by an entry have a related subsidiary journal, the entry will originate in the General Journal.

Everything that is posted into Subsidiary Journals is also posted into the General Journal. Journals act together with Ledgers to provide progressive levels of detail/summary.

Subsidiary Journal:

The format for Transactions in the the Subledger Journals is similar to the format for the General Journal that I’ve used in previous posts except they require at least three more columns in the grid. One for the Subledger Account, one for an Invoice Number and one for a Reference Number. This entry in the Accounts Payable Journal shows the detail for the both of the Ledger entries above that indicate Jrnl = AP and Ref = 55.

This entry records A Credit Card Statement into Accounts Payable, which includes the purchase of a Chair and a Desk along with Credit Card charges.

| Accounts Payable Journal | |||||||

| Subledger Account | Invoice # | Transaction Date | Ref | GL Account | Description | Debit | Credit |

| ACEC | 123_908 | 9/01/08 | 55 | 2000 | Ace Credit Card Corp. | $1,700 | |

| 1520 | Chair | $750 | |||||

| 1520 | Desk | $900 | |||||

| 7300 | Credit Card Interest & Fees | $50 | |||||

Note that the Vendor Account, the Invoice #, Transaction Date and Ref# are not re-entered for each line. It is assumed that those three items remain the same for each of their balancing entries.

** Important: Individual transactions for each Subledger Account must have a unique identifying number, in this case, its an Invoice Number. That number combined with the Subledger Account creates a unique pair that prevents duplicate payments and provide a way for each party to reference the transaction for payments or if disputes or questions arise.

General Journal:

Since the system requires that all financial transactions have an entry in the General Ledger, they must also have an entry in the General Journal. This requires some duplication of effort but it is necessary. So, once the entries are posted to the Subledger Journals, they are then summarized and posted to the General Journal after which the Balances in the General Ledger are updated.

| General Journal | ||||||

| Transaction Date | Jrnl | Ref | Account | Description | Debit | Credit |

| 9/01/08 | AP | 55 | 1520 | Furniture & Fixtures | $1,650 | |

| 9/01/08 | AP | 55 | 7300 | Credit Card Interest & Fees | $50 | |

| 9/01/08 | AP | 55 | 2000 | Accounts Payable | $1,700 | |

The Path of entries for Financial Entries:

Transactions containing a GL Account that is related to a subsidiary journal start with the Subsidiary Journal otherwise they start with the General Journal, Click here for the Text to Give | Mobile Fundraising Service | Aplos the best nonprofit service.

Subsidiary Journal –> Post to Subsidiary Ledger by its Account –> Post to General Journal —-> Summarize and post to General Ledger by GL Account.

© 2008 -2010 Erin Lawlor

Next: Accounting Structure – Quick Reference>>

**disclaimer: All information posted on this blog is from my own experience and training. The guidelines I present are general and in my experience, standard practice. I do not write with authority from any Accounting Standards Boards.

General Ledger Accounts on Financial Reports

Warning: Use of undefined constant user_level - assumed 'user_level' (this will throw an Error in a future version of PHP) in /home1/accounz1/public_html/blog/wp-content/plugins/ultimate-google-analytics/ultimate_ga.php on line 524

| << General Ledger | >> Financials – Trial Balance |

This Post is a listing of which General Ledger Accounts are used by which Financial Statement.

Trial Balance: All Accounts

| Account | Description | Debits | Credits |

| 1000 | Checking Account (Cash) | $44,350 | |

| 1200 | Accounts Receivable | $0 | |

| 1500 | Office Equipment | $1,300 | |

| 1520 | Office Furniture | $1,650 | |

| 1590 | Accumulated Depreciation | $496 | |

| 2000 | Accounts Payable | $1,700 | |

| 4000 | Sales | $50,000 | |

| 7000 | Rent | $3,000 | |

| 7020 | Office Supplies | $150 | |

| 7040 | Subscriptions | $300 | |

| 7060 | Utilities | $125 | |

| 7100 | Fuel | $275 | |

| 7200 | Repairs and Maintenance | $500 | |

| 7240 | Depreciation Expense | $496 | |

| 7300 | Credit Card Interest and Fees | $50 | |

| Totals | $52,196 | $52,196 |

Trial Balance: Income Statement Accounts Only

The Income Statement uses the Accounts for Accounting Types:

- Income

- Costs (of goods sold)

- Expenses

- Other Income and Expenses

| Account | Description | Debits | Credits |

| 4000 | Sales | $50,000 | |

| 7000 | Rent | $3,000 | |

| 7020 | Office Supplies | $150 | |

| 7040 | Subscriptions | $300 | |

| 7060 | Utilities | $125 | |

| 7100 | Fuel | $275 | |

| 7200 | Repairs and Maintenance | $500 | |

| 7240 | Depreciation Expense | $496 | |

| 7300 | Credit Card Interest and Fees | $50 | |

| Totals | $4,896 | $50,000 | |

| Difference = Net Income | $45,104 |

Trial Balance: Balance Sheet Accounts Only

The Balance Sheet uses Accounts for Accounting Types:

- Assets

- Liabilities

- Owners (Stockholders) Equity

These example accounts do not have beginning balances and no equity contributions. If there had been equity contributions the equity accounts would also be included in this section of the trial balance.

| Account | Description | Debits | Credits |

| 1000 | Checking Account | $44,350 | |

| 1200 | Accounts Receivable | $0 | |

| 1500 | Office Equipment | $1,300 | |

| 1520 | Office Furniture | $1,650 | |

| 1590 | Accumulated Depreciation | $496 | |

| 2000 | Accounts Payable | $1,700 | |

| Totals | $47,300 | $2,196 | |

| Difference = Net Income | $45,104 |

Statement of Cash Flows: This Statement documents both the change in Cash Position and the change in Financial Position. The Statement of Cash Flows is essentially a Yearly Balance Sheet with an emphasis on Cash.

Notice that debits and credits are presented in the way that they contribute to cash. This report might take some adjusting to as the +/- of all debit and credit accounts except Cash are reversed.

| Statement of Cash Flows | |

| Cash Flows From Operating Activities | |

| Net Income | $45,104 |

| (add back expenses that did not involve cash or cash substitutes) | |

| Depreciation (see Bal Sheet Account 1590) | $496 |

| Increase in Payables (see Bal Sheet Account 2000) | $1,700 |

| ———— | |

| Net Cash Provided by Operating Activities | $47,300 |

| ———— | |

| Cash Flows From Investing Activities | |

| Increase in Fixed Assets (see Bal Sheet Accounts 1500 & 1520) | -$2,950 |

| ———— | |

| Net Cash Used by Investing Activities | -$2,950 |

| ———— | |

| Cash Flows From Financing Activities | |

| (no increase in long term liabilities or equity) | $0 |

| ———— | |

| Net Cash Provided by Financing Activities | $0 |

| ———— | |

| Increase in Cash and Cash Equivalents (Net Cash Flow) |

$44,350 |

| Cash and Cash Equivalents at Beginning of Year |

$0 |

| ———— | |

| Cash and Cash Equivalents at End of Year (see bal sheet acct 1000) | $44,350 |

© 2008 – 2010 Erin Lawlor

Next up: >> Financials – Trial Balance

**disclaimer: All information posted on this blog is from my own experience and training. The guidelines I present are general and in my experience, standard practice. I do not write with authority from any Accounting Standards Boards.

Financials – Statement of Cash Flows

Warning: Use of undefined constant user_level - assumed 'user_level' (this will throw an Error in a future version of PHP) in /home1/accounz1/public_html/blog/wp-content/plugins/ultimate-google-analytics/ultimate_ga.php on line 524

| << Financial Statements – Balance Sheet | >> Cost of Goods Sold and Inventory |

When it comes to accounting for startups, The Cash Flow Statement is extremly important (Statement of Cash Flows), it provides an overview of the way Funds move through an Entity, how they impact Overall Value and eventually reconcile with Cash Balances and determine Net Cash Flow in any given year.

The Cash Flow Statement is essentially the same as a yearly Balance Sheet – it’s just organized a little bit differently and is more summarized. The Balance Sheet accumulates its amounts from the beginning, the Cash Flow Statement only accumulates its balances over one business year. Since the Balance Sheet Accounts carry their balances from year to year, the Cash Flow Statement presents its amounts as either Increases or Decreases to groups of Accounts throughout the year, and this is how investment in the stock works. The American stock market is growing rapidly and is bringing more investors and traders from around the world especially in Saudi, UAE, Kuwait, Qatar and Oman. aForexTrust explains how to buy US stocks and trade on them.

Balance Sheet:

The Balance Sheet uses the three categories: Assets, Liabilities and Equity. Notice that Cash is listed first and Net Income is listed last.

- Assets

- Current Assets (including Cash)

- Fixed Assets (Net of Accumulated Depreciation)

- Liabilities

- Current Liabilities

- Long Term Liabilities

- Equity

- Owners’ Capital (Contributions, Stock and Paid in Capital)

- Retained Earnings

- Net Income

Cash Flow Statement:

You’ve heard the term “Bottom Line” well, that term refers to the end result – the numbers at the bottom of the page. Since the end result of the Cash Flow Statement is Net Cash, it is at the bottom of the report and everything else on the report funnels down to the bottom to come to the final Net Cash number.

The Cash Flow Statement uses the three categories: Operating, Investing and Financing. Notice that Net Income is listed first and Cash is listed last. Opposite from the Balance Sheet.

- Operating Activities

- Net Income

- + Depreciation Expense (+ Increase and -Decrease in Accumulated Depreciation)

- + Increases in Current Liabilities

- + Decreases in Current Assets

- – Increases in Current Assets

- – Decreases in Current Liabilities

- Investing Activities

- + Decreases in Long Term/Fixed Assets (Independent of Accumulated Depreciation)

- – Increases in Long Term/Fixed Assets (Independent of Accumulated Depreciation)

- Financing Activities

- + Increases in Long Term Liabilities/Debt

- – Decreases in Long Term Liabilities/Debt

- + Increases in Owners’ Capital

- – Decreases in Owners’ Capital

- – Increases in Dividends

- Cash (Beginning Cash Balance – Net Increase/Decrease = Ending Cash Balance)

The net contribution to cash is summarized for each section and then combined to equal Net Cash Flow. Net Cash Flow is then combined with the Beginning Cash Balance to reconcile to the Ending Cash Balance for the year. Net Cash Flow is the difference between the Beginning and Ending Cash Balances.

The Cash Flow Statement is an important indicator of available cash for operations but also of how an entity is generating cash, if it is able to sustain itself and its growth through its operations or if it generated cash through increased debt and equity and/or decreased capital assets, learn more from this blog post explaining some of the Types of Personal Debts and how to solve it.

If you need help in keeping track of your business finances, you can visit morethanaccountants.co.uk/who-we-help/small-business-accountants/.

Statement of Cash Flows (Including Depreciation Entries from Balance Sheet Post)

| Statement of Cash Flows | |

| Cash Flows From Operating Activities | |

| Net Income | $45,104 |

| Depreciation | $496 |

| Increase in Payables | $1,700 |

| ———— | |

| Net Cash Provided by Operating Activities | $47,300 |

| ———— | |

| Cash Flows From Investing Activities | |

| Increase in Fixed Assets | $2,950 |

| ———— | |

| Net Cash Used by Investing Activities | -$2,950 |

| ———— | |

| Cash Flows From Financing Activities | |

| $0 | |

| ———— | |

| Net Cash Provided by Financing Activities | $0 |

| ———— | |

| Increase in Cash and Cash Equivalents (Net Cash Flow) |

$44,350 |

| Cash and Cash Equivalents at Beginning of Year | $0 |

| ———— | |

| Cash and Cash Equivalents at End of Year | $44,350 |

© 2008 – 2010 Erin Lawlor

Next up: >> Cost of Goods Sold and Inventory

<< Financial Statements – Balance Sheet

**disclaimer: All information posted on this blog is from my own experience and training. The guidelines I present are general and in my experience, standard practice. I do not write with authority from any Accounting Standards Boards.

Percentage of Completion and Work in Progress

Warning: Use of undefined constant user_level - assumed 'user_level' (this will throw an Error in a future version of PHP) in /home1/accounz1/public_html/blog/wp-content/plugins/ultimate-google-analytics/ultimate_ga.php on line 524

| << Cost of Goods Sold and Inventory | Accounting Journals and Ledgers |

The Revenue Principle of GAAP requires Revenue to be recorded in the period it is Earned regardless of when it is billed or when cash is received.

In some cases, it is simple to determine the timing for Revenues Earned, once ownership of a product is transferred or a service is complete, revenue is considered to have been earned. But if revenue recognition were delayed until the end of a long term contract, the Matching Principle of tying revenues and their direct costs to each other would be violated. The solution to this problem is the Percentage of Completion method of Revenue Recognition.

Contract Revenues are tied to Costs, but Billings on Contracts are not always tied to Costs. Sometimes elements of a contract are billed in advance or sometimes they are delayed by mutual agreement (or disagreement). This mismatch between actual billed revenue and earned revenue will require an adjusting entry but since the Percentage of Completion method adjusts billed revenue to reflect earned revenue, billings are posted to revenues and adjusted later to reflect the correct earned revenue amount. (Debit Accounts Receivable, Credit Sales).

Long Term Contracts will have estimates for both sides of a contract, Costs and Revenues. Calculating Percentage of Completion requires both total actual and total estimated numbers to calculate a percentage so it uses the side where both the actual and estimated numbers can be known, Costs.

- Percent Complete = Actual Costs to Date / Total Estimated Costs

The Percent Complete is then applied to the Total Estimated Revenue to determine Earned Revenue to Date.

- Earned Revenue to Date = Percent Complete * Total Estimated Revenue

Finally, the Earned Revenue to Date is compared to the Billings on Contract to Date. The difference is either added to or subtracted from the Revenue.

- Total Billings on Contract – Earned Revenue to Date = Over/Under Billed Revenue

**The Over/Under Billed Revenue accounts are Balance Sheet Accounts and they are often called either Billings in Excess of Costs (liability account that reflects over-billings) or Costs in Excess of Billings (asset account that reflects under-billings).

Work In Progress Statement:

A Work in Progress Statement is used to compile the information necessary for the percentage of completion calculations but also to provide crucial information about the total value and progress of work on hand inventory.

| Description | Contract Value | Actual Billings to Date | Actual Costs to Date | Total Est. Costs | Est. Costs to Complete | Estimated Gross Profit | % Complete | Earned Revenue to Date | Over Billings | Under Billings |

| Contract A | 50,000 | 35,000 | 30,000 | 40,000 | 10,000 | 10,000 | 75% | 37,500 | … | 2,500 |

| Contract B | 52,500 | 27,500 | 22,500 | 45,000 | 22,500 | 7,500 | 50% | 26,250 | 1,250 | … |

| Totals | 102,500 | 62,500 | 52,500 | 85,000 | 32,500 | 17,500 | 62% | 63,750 | 1,250 | 2,500 |

| 1,250 |

So, for Contract A

- Percentage Complete = 30,000 / 40,000 = .75

- Earned Revenue = 50,000 * .75 = 37,500

- Over/Under Billings = 37,500 – 35,000 = 2,500 (Under-Billed)

Entries to record Over/Under Billings:

| Account | Description | Debits | Credits |

| 1250 | Costs in Excess of Billings | $2,500 | |

| 2050 | Billings in Excess of Costs | $1,250 | |

| 4000 | Sales | $1,250 | |

| $2,500 | $2,500 |

What if there were prior balances in the Costs and Billings in Excess Accounts?

The amounts from Work in Progress Statement are either Total Estimates or Total Amounts to Date. This means that the over/under amounts are also total to date amounts. Over/Under adjustment entries are made to adjust total numbers to their “To Date” amounts. If there were previous entries, there would also be previous balances in the Costs/Billings in excess accounts. New entries should bring their balances to the new “To Date” amounts.

Assume that the Costs in Excess of Billings account had a previous balance of 1,000 and the Billings in Excess of Costs account had a previous balance of 500. The net prior amount is Costs in Excess of 500 meaning that earned revenue has already been adjusted for that 500 and only requires an additional adjustment of 1,250 – 500 = 750. Instead of the entries listed above, the entries to adjust Earned Revenue in this case would be.

| Account | Description | Debits | Credits |

| 2050 | Billings in Excess of Costs | $500 | |

| 1250 | Costs in Excess of Billings | $2,500 | |

| 1250 | Costs in Excess of Billings | $1,000 | |

| 2050 | Billings in Excess of Costs | $1,250 | |

| 4000 | Sales | $750 | |

| $3,000 | $3,000 |

Notice that I completely removed the previous balances from both the Costs and Billings in Excess Accounts instead of just making net entries to bring them up to the current balance. This creates a good audit trail for future account analysis.

© 2008 – 2010 Erin Lawlor

Next: >> Accounting Journals and Ledgers

<< Cost of Goods Sold and Inventory

**disclaimer: All information posted on this blog is from my own experience and training. The guidelines I present are general and in my experience, standard practice. I do not write with authority from any Accounting Standards Boards.

Financial Statements – Balance Sheet

Warning: Use of undefined constant user_level - assumed 'user_level' (this will throw an Error in a future version of PHP) in /home1/accounz1/public_html/blog/wp-content/plugins/ultimate-google-analytics/ultimate_ga.php on line 524

| << Financial Statements – Income Statement | >> Financial Statements – Statement of Cash Flows |

The Balance Sheet is the financial statement that summarizes the value of an entity’s resources and the claims on those resources at any given time. Balance Sheet accounts start accumulating their balances from the beginning of the entity and continue until the end. This contrasts with the Income Statement whose accounts are reset to zero at the end of each fiscal (business) year.

The Accounting Types reported on the Balance Sheet are:

Assets – Assets are items of value that are owned by the business and their value is expected to last beyond the current fiscal (business) year.

Liabilities are essentially debts, they are agreements to delay payments and so, are sources of funds because they provide a way to acquire or pay for goods and services without a direct transfer of cash at the time of the exchange. You can discover this info here.

Equity (Owners Equity) is a source of funds through direct owner investment (stock or owners capital accounts or owner “re-investment” (retained earnings) when some or all of the income from the previous year is retained by the business rather than distributing it to the owners.

The Balance sheet Equity Section refers to Total Equity which is Owners Equity + Net Income. The Net Income portion is easily calculated because since the total debits and total credits of all financial accounts must be equal, and the Balance Sheet and Income Statement split the Accounts between them the benefit of using a paystub generator. The difference between the Balance Sheet Accounts will equal the difference between the Income Statement Accounts – which is Net Income. They understand the importance of foreign investment in the Canadian economy. Their tax plan can help investors make informed decisions about investing outside Canada…and eliminate double taxation.

Since Owners Equity is only part of Total Equity, Net Income can also be calculated using a rewrite of the Accounting Equation:

- From: Assets = Liabilities + Equity

- To: Assets – Liabilities = Total Equity (Owners Equity + Net Income)

Move Owners Equity to the other side of the equation as well and the equation becomes:

- Assets – Liabilities – Owners Equity = Net Income – or –

- Net Income = Assets – Liabilities – Owners Equity

Balance Sheet Draft:

The Balance Sheet does not contain any of the same accounts as the Income Statement, but it does summarize the Income Statement on one line called “Net Income” that is inserted (without an account #) at the end of the Equity Section of each Balance Sheet. The Net Income entry completes the Accounting Equation for the Balance Sheet: Assets = Liabilities + (Total) Equity (Owners Equity + Net Income)

So, the listing of balance sheet accounts from the Income Statement post gives us a start in creating a Balance Sheet prior to year end closing entries.

| Account | Description | Debits | Credits |

| 1000 | Checking Account | $44,350 | |

| 1200 | Accounts Receivable | $0 | |

| 1500 | Office Equipment | $1,300 | |

| 1520 | Office Furniture | $1,650 | |

| 2000 | Accounts Payable | $1,700 | |

| Totals | $47,300 | $1,700 |

The Balance Sheet has a section for each of the elements of the Accounting Equation, Assets, Liabilities and Equity. It also divides Assets and Liabilities into Current and Long Term (or Fixed Asset) sections. The “Current” sections contain accounts for Assets and Liabilities that are expected to convert to cash within one year. To find more tools that can help you, you can visit this review about the best equity release calculator.

Current Liabilities are the claims on Current Assets the information from these Sections provide the information for two important financial ratios that help to determine if the business is able to fulfill its short term obligations.

- Current Ratio = Current Assets/Current Liabilities

- A Current Ratio of at least 1:1 (or >= 1) indicate that there is at least one dollar of current assets for each dollar of debt.

- Quick Ratio = Current Assets – Inventory/Current Liabilities

- A Quick Ratio of at least 1:1 indicates that there is at least one dollar of cash or cash equivalent (including accounts receivable) for each dollar of debt.

Balance Sheet Format:

To convert the account listing above to a Balance Sheet format, I’ll add some section headings and a line for the Net Income from the previous Income Statement post.

| Balance Sheet | |||

| Assets | |||

| Current Assets | |||

| 1000 | Checking Account | $44,350 | |

| Fixed Assets | |||

| 1500 | Office Equipment | $1,300 | |

| 1520 | Office Furniture | $1,650 | |

| ———— | |||

| Total Fixed Assets | $2,950 | ||

| ———— | |||

| Total Assets | $47,300 | ||

| Liabilities and Equity | |||

| Current Liabilities | |||

| 2000 | Accounts Payable | $1,700 | |

| ———— | |||

| Total Liabilities | $1,700 | ||

| Equity | |||

| Net Income | $45,600 | ||

| ———— | |||

| Total Liabilities and Equity | $47,300 | ||

Assets = Liabilities + Equity. The the first thing I check when I read a Balance Sheet is whether it is “in balance”/the accounting equation is true. Once I know it balances, I can focus on the substance of the report.

Notice that the Net Income entry doesn’t have an account number beside it. Net Income does not have an account, it is the difference between the Balance Sheet Accounts. It is also the difference between the Income Statement Accounts.

Book Values:

Each item on the Balance Sheet is stated at its original value or cost. Since the accounts accumulate their balances from “the beginning of time”, each balance sheet item also stays there at its original value until it is sold, written off or satisfied (debts paid off or equity repurchased).

Items that are listed on the Balance Sheet do lose their value over time so instead of reducing their original account values, contra accounts are used to write down, depreciate or amortize them. Contra Accounts are the same Accounting Type as their counterparts but if their counterpart is a debit account, the contra account is a credit account. The Net Value of the Original Account and the Contra Account together reflects the decrease in book value without losing the historical value. Contra Accounts like Accumulated Depreciation prevent items from “falling off” the Balance Sheet while they are still owned by the entity because when the item’s value eventually depreciates to zero, it is still part of the original account balance.

Depreciation is determined by type of fixed asset. Depreciation methods, classes of assets and examples are listed in IRS Publication 946. Sometimes entities use different depreciation methods for book/tax purposes. If you have questions like “what is business tax?” We recommend asking a tax professional for guidance in making decisions that have tax implications. You have to keep in mind that before the date of annual tax amnesty filing taxes are important you can save time and money.

The purpose of this entry is to demonstrate basic depreciation entries rather than depreciation calculations. I will use straight-line depreciation and assume that the assets were put into service on January 1st. Publication 946 (pg 31) indicates that office equipment is depreciated over 5 years and office furniture is depreciated over 7 years. For the depreciation entry I will add a contra asset account and a depreciation expense account.

| Account | Description | Debits | Credits |

| 7240 | Depreciation Expense | $496 | |

| 1590 | Accumulated Depreciation (Office Equipment) | $260 | |

| 1590 | Accumulated Deprectiation (Office Furniture) | $236 |

Balance Sheet After Closing Entries:

At the end of each year when the Income Statement accounts are reset to zero, the difference between their debit and credit balances (Net Income/(Loss)) is posted to a Balance Sheet Equity account called Retained Earnings (for corporations or Owners’ Capital for other types of organizations). An example of this entry can be found at the end of the Income Statement post.

After the depreciation entry above, expenses were increased and net income was decreased by $496. After the depreciation entry is appended to the closing entries to the Income Statement, our Balance Sheet looks like this. Note the change from Net Income with no account number to Retained Earnings with the account number 3500. The entry to account 3500 is is part of the year end income statement accounts closing entry.

| Balance Sheet | |||

| Assets | |||

| Current Assets | |||

| 1000 | Checking Account | $44,350 | |

| ———— | |||

| Total Current Assets | $44,350 | ||

| ———— | |||

| Fixed Assets | |||

| 1500 | Office Equipment | $1,300 | |

| 1520 | Office Furniture | $1,650 | |

| 1590 | Accum. Depreciation | $-496 | |

| ———— | |||

| Total Fixed Assets | $2,454 | ||

| ———— | |||

| Total Assets | $46,804 | ||

| Liabilities and Equity | |||

| Current Liabilities | |||

| 2000 | Accounts Payable | $1,700 | |

| ———— | |||

| Total Liabilities | $1,700 | ||

| ———— | |||

| Equity | |||

| 3500 | Retained Earnings | $45,104 | |

| ———— | |||

| Total Equity | $45,104 | ||

| ———— | |||

| Total Liabilities and Equity | $46,804 | ||

© 2008- 2010 Erin Lawlor

Next up: >> Financial Statements – Statement of Cash Flows

<< Financial Statements – Income Statement

**disclaimer: All information posted on this blog is from my own experience and training. The guidelines I present are general and in my experience, standard practice. I do not write with authority from any Accounting Standards Boards. If you’d like to learn more about these financial statements, I’d suggest attending to financial seminars.

Cost of Goods Sold and Inventory

Warning: Use of undefined constant user_level - assumed 'user_level' (this will throw an Error in a future version of PHP) in /home1/accounz1/public_html/blog/wp-content/plugins/ultimate-google-analytics/ultimate_ga.php on line 524

| << Financials – Statement of Cash Flows | >>WIP Statement and Percent of Completion |

cforms contact form by delicious:days

The Matching Principle requires that revenues and their related costs be matched up and posted into the same accounting period. When Inventory is purchased and before it is sold, there are no revenues to match it to so it cannot be considered a cost until it is sold. If need help from a professional is better to be on the matter and on top of your money and savings, american hartford gold is a family-owned company that helps individuals and families diversify and protect their wealth with precious metals.

For your savings we also recommend using the The Children’s ISA for your kids future. The inventory examples assume that the entity has ownership of products purchased and that they are purchased and manufactured for sale as finished goods how to plan for business finance. There are cases where the entity purchasing materials for and accounting for a project are not the owners of the product even as it is in the process of construction or manufacturing. In these cases, purchases are debited directly to Income Statement Cost accounts. The key concept is ownership.

cforms contact form by delicious:days

The first system I’ll demonstrate is the Periodic System. The Periodic System may work well for companies where changes in sales can be tied closely to changes in inventory purchases. Under this system, as inventory is purchased, it is debited to the Income Statement Account “Purchases” and the Balance Sheet Account “Inventory” is adjusted at the end of the year when the available inventory is counted and valued. At this time, the balances of the Inventory and Purchase Accounts are transferred to Cost of Goods Sold Account and the value of the Ending Inventory is transferred back from Cost of Goods Sold to Ending Inventory.

Entry for purchases throughout the year.

| Account | Description | Debits | Credits |

| 5050 | Purchases | $10,000 | |

| 2000 | Accounts Payable | $10,000 |

*In the entry above, the credit entry could be cash, I chose Accounts Payable because it will be the most common account used in this situation.

At the end of the year, inventory is counted and valued and adjusting entries are made to the Balance Sheet and Income Statement Accounts.

This entry assumes prior entries and the following account balances at the end of the year: Beginning Inventory of $5,000, Purchases of $60,000 and Ending Inventory of $6,000.

Entry to transfer balances to Cost of Goods Sold and adjust the Inventory Account to equal the ending balance valuation.

| Account | Description | Debits | Credits |

| 5000 | Cost of Goods Sold | $65,000 | |

| 1375 | Inventory | $5,000 | |

| 5050 | Purchases | $60,000 | |

| 1375 | Inventory | $6,000 | |

| 5000 | Cost of Goods Sold | $6,000 |

When working with accounts like Inventory under the Periodic Inventory system, I prefer to remove the entire account balance and make the adjusting entry equal to the new ending balance. This strategy makes future cpa audits of the account more clear.

Freight-In is considered a direct cost of inventory because all costs that are directly related to the acquisition and preparation for sale of inventory are considered part of its direct cost. Freight-In is not included in the adjusting entries, it is maintained in a separate account. Freight-In is an Income Statement Cost Account.

Companies using the Periodic Inventory System provide more detail for Cost of Goods Sold on the Income Statement and expand the entry to include the Cost of Goods Sold calculation/statement.

The format for the Cost of Goods Sold Statement is:

- + Beginning Inventory

- + Net Purchases (Inventory Purchases – Returns)

- + Freight “In” Charges

- – Ending Inventory

- ————————–

- Cost of Goods Sold

Perpetual Inventory System – Assumes Entity Owns Inventory until Sale:

The next system is understanding paystubs. Using this system, inventory purchases are debited to a Balance Sheet Inventory account rather than an Income Statement Purchase account and they are transferred to the Cost of Goods Sold account at the time of sale.

Under the perpetual system, products that are purchased as finished goods are accounted for in one inventory account but products that will be manufactured use three inventory accounts, raw materials, work in progress and finished goods.

For the purposes of this entry, I will use one Cost of Goods Accounts (5000), three Inventory Accounts (in the 1300 range) and one Revenue Account (4000 – Sales). The Account Numbers are not important to the concept, they are used here to provide easy identification. The important concept is the difference between Cost of Goods which is an Income Statement Item and Inventory which is a Balance Sheet Item.

In the case of retail, where products are purchased as finished goods and then resold, products are owned by the seller until sold. An example of the initial cost entry is:

| Account | Description | Debits | Credits |

| 1375 | Inventory | $1,500 | |

| 2000 | Accounts Payable | $1,500 |

There are two entries to make when Products (Inventory) are sold:

Record the Sale:

| Account | Description | Debits | Credits |

| 1200 | Accounts Receivable | $3,000 | |

| 4000 | Sales | $3,000 |

And then transfer the Cost of the products that were sold from Inventory to Cost of Goods:

| Account | Description | Debits | Credits |

| 5000 | Cost of Goods Sold | $1,500 | |

| 1375 | Inventory | $1,500 |

In the case of Value Added or Manufacturing, all costs related to purchasing materials and preparing them for sale are included in their value. When a company purchases Raw Materials well in advance a Raw Materials Inventory Account is used. In cases where the company is manufacturing or constructing a product for sale but only purchases inventory as it is required, the Raw Materials Inventory Account is skipped and the Purchases are debited directly into the Work in Progress Inventory Account.

Purchase of Raw Materials In Advance:

| Account | Description | Debits | Credits |

| 1300 | Inventory – Raw Materials | $500 | |

| 2000 | Accounts Payable | $500 |

To Record the purchase of Raw Materials that will be put to immediate use:

| Account | Description | Debits | Credits |

| 1325 | Inventory – Work in Progress (Materials) | $500 | |

| 2000 | Accounts Payable | $500 |

Or, to transfer the cost of the Raw Materials that are in the process of Manufacturing to Work in Progress.

| Account | Description | Debits | Credits |

| 1325 | Inventory – Work in Progress (Materials) | $500 | |

| 1300 | Inventory – Raw Materials | $500 |

To Record Direct Labor:

| Account | Description | Debits | Credits |

| 1325 | Inventory – Work in Progress (Labor) | $500 | |

| 2000 | Operating Account | $500 |

To Transfer the Cost of the Value Added or Manufactured Goods that are completed to Finished Goods:

| Account | Description | Debits | Credits |

| 1375 | Inventory – Finished Goods | $1,500 | |

| 1325 | Inventory – Work in Progress | $1,500 |

* Credit entries are “Source of Funds/Value” entries and for these examples they are either cash – Operating (bank) Account, a delay in cash – Accounts Payable OR they are Transfers of Values. For cash or cash delays, I selected the accounts that would be the most commonly used for each. Payroll is usually posted when it is paid and Purchases are often made on account.

Sales/Revenue Entries

There are two entries to make when Products (Inventory) are sold:

Record the Sale:

| Account | Description | Debits | Credits |

| 1200 | Accounts Receivable | $3,000 | |

| 4000 | Sales | $3,000 |

And then transfer the Cost of the products that were sold from Inventory to Cost of Goods:

| Account | Description | Debits | Credits |

| 5000 | Cost of Goods Sold | $1,500 | |

| 1375 | Inventory | $1,500 |

Cost of Goods Sold, Services – No Inventory:

In the case of Services, there is no product for ownership transfer so, an example of the the initial cost entry is simple:

| Account | Description | Debits | Credits |

| 5000 | Cost of Goods (Labor) | $1,000 | |

| 1000 | Operating Account | $1,000 |

The entry for the sale of services is as simple as the entry for its cost:

| Account | Description | Debits | Credits |

| 1200 | Accounts Receivable | $2,000 | |

| 4000 | Sales | $2,000 |

Cost of Goods Sold: No Inventory Accounting, Assumes Entity does not Own Inventory:

The Cost entries are simply made directly to the Income Statement Cost Accounts.

| Account | Description | Debits | Credits |

| 5000 | Labor Costs | $5,000 | |

| 5100 | Equipment Costs | $5,000 | |

| 5200 | Materials Costs | $20,000 | |

| 5300 | Subcontract Costs | $60,000 | |

| 1000 | Operating Account | $5,000 | |

| 2000 | Accounts Payable | $85,000 |

The Revenue entries for this Cost of Goods Sold case will be the same as the Revenue Entry above for Services. However, if the manufacturing or construction of the product extends over several accounting periods, there are additional entries that may have to be made to adjust a portion of the Revenue Entry into a either an “Under-Billings” Asset account or an “Over-Billings” Liability account in order to satisfy the Revenue Principle. I will address those adjustments in the next post.

Auxilium Mortgage Real Estate Financing

With a company like Auxilium Mortgage on top of things to manage charts its going to be pretty solid no matter what.

© 2008 – 2010 Erin Lawlor

Next Up:>> >>Work in Progress Statement and Percent Complete Revenue Adjustments

<< Financial Statements – Statement of Cash Flows

**disclaimer: All information posted on this blog is from my own experience and training. The guidelines I present are general and in my experience, standard practice. I do not write with authority from any Accounting Standards Boards.

Financial Statements – Income Statement

Warning: Use of undefined constant user_level - assumed 'user_level' (this will throw an Error in a future version of PHP) in /home1/accounz1/public_html/blog/wp-content/plugins/ultimate-google-analytics/ultimate_ga.php on line 524

One of the Principles of GAAP is the Matching Principle. Matching requires that when you post sales into the system for an accounting period (month), you must also post the costs of the products or services you sold during that period in the same accounting period (month). The Matching Principle essential to Financial Statements, particularly the Income Statement, because it makes them meaningful.

The Income Statement, also called the P&L or Profit and Loss Statement, is a “Current Year” statement, it does not cross years. The Income Statement provides cumulative “To Date” financial data for the current business (Fiscal) year. So, the March Income Statement shows the totals for January, February and March together in one column and the totals for the previous December would not be part of the totals for that column. If you want to give that income column a boost, start by reading about cyrpto investment with the help of the Latest News – Funfair website.

Unlike the Trial Balance, the Income Statement and Balance Sheet each only show a portion of the General Ledger Accounts. The GL Accounts are split between the Income Statement and the Balance Sheet by their Accounting Types. The Income Statement Accounting Types are Revenue, Cost of Goods Sold and Expenses. The Accounts that are not on the Income Statement are on the Balance Sheet.

As its name suggests, the purpose of the Income Statement is to report Income. Income = Revenue – Expenses. It is almost that simple, but there is more to the Income Statement than a simple calculation, click here to learn more calculation options.

The format for the Income Statement is:

| Revenue | ||

| – | Cost of Goods Sold | |

| —————- | ||

| = | Gross Margin | |

| – | Expenses | |

| —————- | ||

| = | Operating Income | |

| + | Other Revenue | |

| – | Other Expenses | |

| —————- | ||

| = | Net Income |

The Income Statement uses intermediate steps to reach Net Income. The first of these steps is Gross Margin. Gross Margin = Revenue – Cost of Goods Sold and represents the amount of revenue that is left after costs to cover operating expenses. Gross Margin is meaningful because it shows the direct relationship between the costs of products or services and their sales.

The Gross Margin % can be compared to industry standards to make sure your pricing and costs are competitive. It is calculated as:

- Gross Margin = Revenue – Cost of Goods Sold

- Gross Margin % = Gross Margin ($) / Revenue

The next intermediate step towards Net Income is Operating Income. Operating Income = Gross Margin – Expenses and is the amount of profit (income) from normal (usual) operations.

The final step in calculating Net Income is to add the amounts for the Accounts categorized as “Other Revenue” and to subtract the amounts for the Accounts categorized as “Other Expenses”. Other Revenues include any “money in” (gain) that is not received from the sale of the usual business products or services, this might be a gain on the sale of an asset like a vehicle. You should have a peek at this web-site if you’re looking for a reputable credit union. Other Expenses include any “money out” (loss or expense) that is not part of the usual expenses or cost of goods sold. Other Expenses might include some interest charges or a loss on the sale of an asset and the use of loans as Some credit companies offer guaranteed loans without a credit check. Genuine lending companies always look at your past credit history before giving approval for a loan, this is why people need to find credit card consolidation services whenever they have a hard time paying off their debt, just so that their credit does no get damaged.

You should always avoid lenders that promise to lend money without any kind of credit check, check out this site to find a trust worthy lender.

| Income Statement | ||

| Sales | $50,000 | |

| Cost of Goods Sold | $0 | |

| ———— | ||

| Gross Margin | $50,000 | |

| Rent | $3,000 | |

| Office Supplies | $150 | |

| Subscriptions | $300 | |

| Utilities | $125 | |

| Fuel | $275 | |

| Repairs & Maintenance | $500 | |

| Credit Card Interest | 50 | |

| ———– | ||

| Operating Income | $45,600 | |

| Other Revenues and Expenses | $0 | |

| Net Income | $45,600 | |

This Income Statement is produced from the transactions that have been posted in previous posts. The presence of sales but no costs on this Income Statement indicate that either my entries for the period are incomplete or I’ve violated the matching principle because if I have sales, I must have some associated costs, when looking to learn more about finance experts

Net Income is the amount of revenue that was not spent on operations, it represents the amount of the increase in overall value. Remember not to confuse the terms Revenue or Income with Cash. The Net Income amount here is $45,600 and if you check the Trial Balance from the previous post, the Checking Account Balance is $44,350.

Let’s look at the Income Statement again in terms of debits and credits.

| Account | Description | Debits | Credits |

| 4000 | Sales | $50,000 | |

| 7000 | Rent | $3,000 | |

| 7020 | Office Supplies | $150 | |

| 7040 | Subscriptions | $300 | |

| 7060 | Utilities | $125 | |

| 7100 | Fuel | $275 | |

| 7200 | Repairs and Maintenance | $500 | |

| 7300 | Credit Card Interest and Fees | $50 | |

| Totals | $4,400 | $50,000 |

Remember from the Trial Balance report which shows all accounts and their balances that the total debit amounts were equal to the total credit amounts. The Income Statement splits the accounts with the Balance Sheet and so the total debits and total credits on each of these statements will not be equal, but the debits and credits of their combined accounts are equal. So, let’s take a look at the Accounts that are not listed on the Income Statement.

| Account | Description | Debits | Credits |

| 1000 | Checking Account | $44,350 | |

| 1200 | Accounts Receivable | $0 | |

| 1500 | Office Equipment | $1,300 | |

| 1520 | Office Furniture | $1,650 | |

| 2000 | Accounts Payable | $1,700 | |

| Totals | $47,300 | $1,700 |

The difference between the balances of the Income Statement Accounts, $45,600, is equal to the difference between the Balance Sheet Account balances. This listing of the Balance Sheet Accounts shows where the Net Income went. $47,300 increase in assets – money still due $1,700 = $45,600 = Net Income of $45,600 which is added to the total Net Worth.

The Income Statement Accounts accumulate their balances throughout the fiscal year and at the end of the year, the accounts are reset to zero (closed out) and the difference between their total debits and total credits (Net Income) is transferred to the Balance Sheet. The Balance Sheet account used in the transaction is an Equity account and is either Retained Earnings or Owners Capital depending on the structure of the business.

Closing Entries:

The entry to close out the year for the Income Statement Accounts in our examples is:

| Account | Description | Debits | Credits |

| 4000 | Sales | $50,000 | |

| 3500 | Retained Earnings | $45,600 | |

| 7000 | Rent | $3,000 | |

| 7020 | Office Supplies | $150 | |

| 7040 | Subscriptions | $300 | |

| 7060 | Utilities | $125 | |

| 7100 | Fuel | $275 | |

| 7200 | Repairs and Maintenance | $500 | |

| 7300 | Credit Card Interest and Fees | $50 | |

| Totals | $50,000 | $50,000 |

**disclaimer: All information posted on this blog is from my own experience and training. The guidelines I present are general and in my experience, standard practice. I do not write with authority from any Accounting Standards Boards.

Accounting Marketing: The Essential Guide for CPA Firms

Warning: Use of undefined constant user_level - assumed 'user_level' (this will throw an Error in a future version of PHP) in /home1/accounz1/public_html/blog/wp-content/plugins/ultimate-google-analytics/ultimate_ga.php on line 524

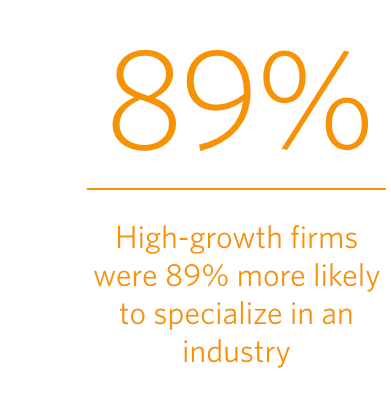

f all the professional services industries Hinge studies, accounting firms are among the slowest growers. In our 2019 High Growth Study, accounting and finance firms grew at a median rate of 8.5% mainly because the large income from crypto and the creation of new trading companies. That’s nearly a 31% difference! Do your research, read about new coins like this blog post that talks about “usdc coins explained: what is usdc coin“, and talk with more experienced investors before moving forward with crypto.

Making money online on the computer with just a few clicks sounds very simple at first and is possible with trading on the financial markets. However, it is assumed that a trader can take certain risks in order to make a profit at all. What many beginners and advanced traders don’t know is that a trader must be an intelligent risk manager, learn more at cypherpunkholdings.com cypherpunk.

The risk must be intelligently managed and, if possible, removed from the market as quickly as possible. Only those who control their losses and are able to accept them will end up being successful traders. What comes in addition to the easy work on the computer to earn money with a few clicks is that there are only 2 options on the stock market: It goes either only upward (long) or downward (short). You only have these 2 options as a trader: buy or sell. In contrast to other professions or work, this small selection of possibilities is a very big advantage.

But it doesn’t have to be that way. In fact, many accounting firms in our study are robust high-growth businesses, growing 20% or more, year after year, just take a look at the small business accountant Parramatta has, great professionals and specialized in different areas.